What Are Managed Accounts? A Guide to Personalized Investment Strategies

Learn what are managed accounts and how they provide tailored investment solutions for both traditional and digital assets. Optimize your portfolio today!

Oct 9, 2025

generated

what are managed accounts, sma investing, investment management, crypto investing, financial planning

When you hear the term "managed account," think of it as the investing equivalent of having a suit custom-made by a tailor. Instead of selecting an off-the-rack option that fits reasonably well—like a mutual fund—a professional money manager builds an investment portfolio from scratch, designed to align perfectly with your financial objectives.

It's a structure that gives you direct ownership of every single asset, whether that's stocks, bonds, or digital assets like BTC and stablecoins. This direct ownership is a critical feature, offering a level of transparency and control that is unavailable in pooled investment funds.

Unpacking the Core Concept of Managed Accounts

At its heart, a managed account is a bespoke investment solution. With mutual funds or ETFs, an investor's capital is pooled with thousands of others' to buy a standardized collection of securities. A managed account is different; it's yours and yours alone. A dedicated manager or advisor constructs a portfolio after gaining a thorough understanding of your unique circumstances.

This personalized approach typically involves several key elements:

A Strategy Built For You: The manager crafts an investment plan reflecting your specific risk tolerance, time horizon, and goals—whether you're focused on capital preservation, income generation, or aggressive growth.

Direct Ownership of Assets: This is a crucial distinction. You don't own "shares of a fund"; you own the individual securities in your account. This provides clearer insight and more influence over your holdings.

Active Professional Management: An experienced manager continuously monitors your portfolio, making tactical adjustments and rebalancing as market conditions or your personal situation changes.

A managed account removes your portfolio from the crowd. It’s a departure from the one-size-fits-all model, allowing for a strategy that can be finely tuned to your exact needs, including specific tax situations or ethical investing mandates.

This model was once reserved for institutional or ultra-high-net-worth investors, but this has changed dramatically. The global retail managed accounts industry has seen significant expansion, now holding an estimated $11 trillion in assets. This growth has been fueled by technological advancements and declining fee structures, making these personalized solutions accessible to a much wider audience. You can learn more about the growth of managed accounts and their market size to understand their increasing prevalence.

Here's a concise summary of the essential elements that define a managed account.

Managed Account Core Features at a Glance

Feature | Description |

|---|---|

Personalization | The investment strategy is tailored to the individual's specific financial goals, risk tolerance, and personal circumstances. |

Professional Management | A dedicated money manager or advisor actively oversees and makes decisions for the portfolio. |

Direct Asset Ownership | The investor directly owns the individual securities (stocks, bonds, etc.) within the account, not shares of a fund. |

High Transparency | Since the investor owns the assets directly, they have a clear view of all holdings, transactions, and associated costs. |

Fee-Based Structure | Compensation is typically a percentage of the assets under management (AUM), aligning the manager's success with the client's. |

These features combine to create a powerful and flexible investment vehicle.

In this guide, we'll examine how these accounts function, compare them against other investment options, and explore their application in the digital asset space for sophisticated BTC and stablecoin strategies.

How a Managed Account Works Step By Step

What actually happens when you open a managed account? The process is more collaborative and structured than simply transferring capital. It is less like buying a generic, off-the-shelf product and more like commissioning a custom-built piece of equipment.

The entire process is designed for transparency, starting with a deep dive into your financial situation and culminating in a portfolio that is actively managed exclusively for you.

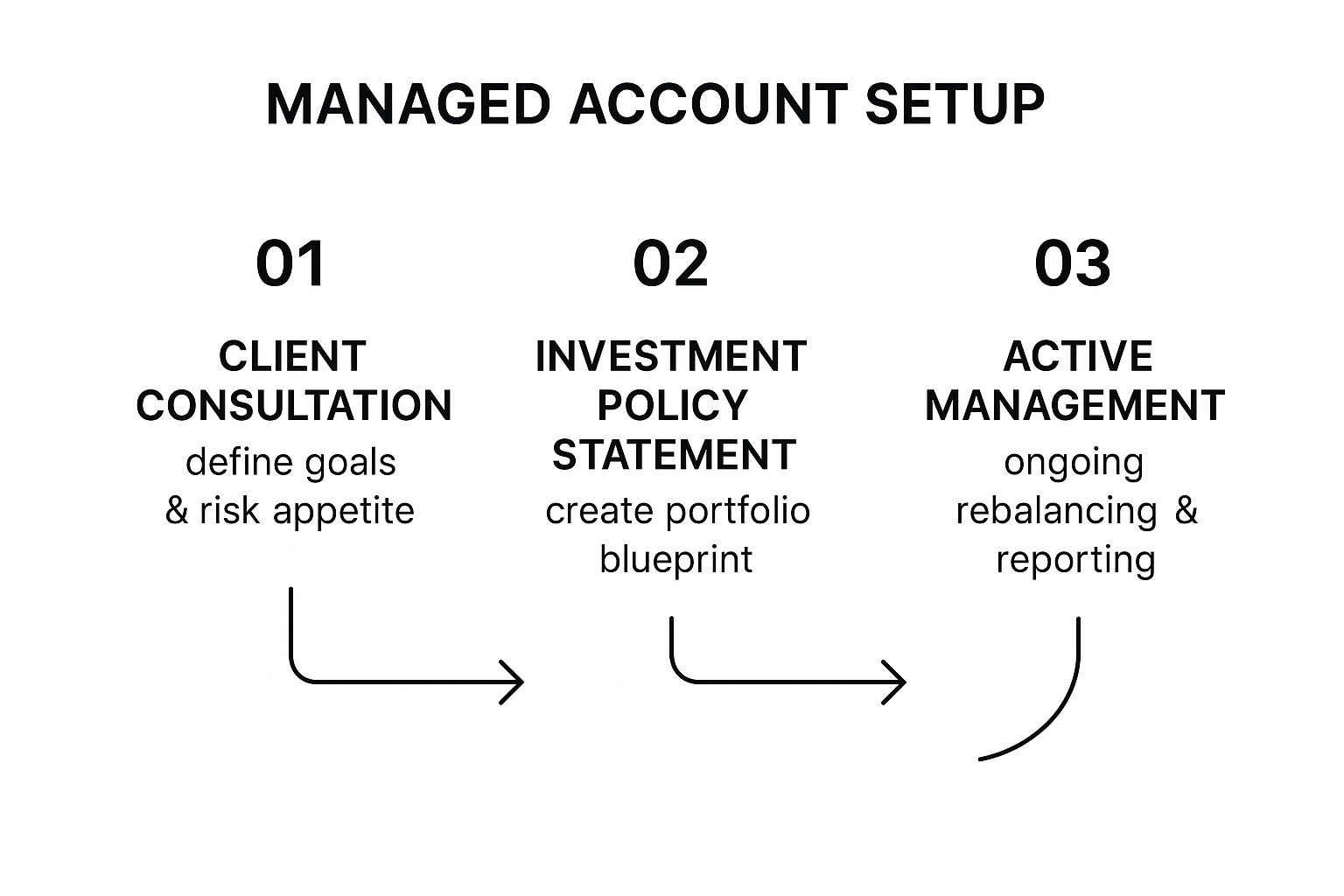

The Foundational Consultation and Blueprint

Everything begins with a detailed consultation with a financial advisor or wealth manager. This is a discovery session focused on specifics: your financial goals, investment horizon, liquidity needs, and—critically—your comfort level with risk. This conversation lays the groundwork for all subsequent decisions.

From that consultation, the manager drafts a critical document called the Investment Policy Statement (IPS). The IPS functions as the constitution for your portfolio. It is a formal agreement that outlines the strategic plan, including objectives, any restrictions, and the specific asset allocation strategy the manager will adhere to.

The IPS serves two key purposes:

It ensures you and the manager are in full alignment before any capital is deployed.

It creates a clear benchmark, making it straightforward to measure the performance of both the account and the manager over time.

This infographic breaks down the typical flow, from the initial meeting to day-to-day management.

As illustrated, a managed account isn't a one-time setup; it is an ongoing relationship built on a clearly defined mandate.

Active Management and Reporting

With the IPS signed off, the real work begins. Your manager, whether focused on traditional markets or a specialized crypto strategy, will start constructing your portfolio based on that blueprint. They purchase the actual securities—stocks, bonds, or digital assets—and hold them directly in an account under your name. That direct ownership is what gives managed accounts such a high degree of transparency.

From this point forward, the manager is responsible for:

Ongoing Monitoring: Closely tracking markets and the performance of every asset in your portfolio.

Strategic Rebalancing: Making periodic adjustments to your holdings to bring your asset mix back in line with the IPS targets.

Performance Reporting: Providing you with regular, detailed reports showing exactly what you own, every transaction made, and how your portfolio is performing.

This continuous oversight is where the real value lies. A professional manager is compensated for navigating market volatility, capitalizing on opportunities, and managing risk according to the pre-agreed rules. It’s a level of focus that is unattainable in a large-scale, one-size-fits-all fund.

Managed Accounts vs. Mutual Funds and ETFs

To fully understand managed accounts, it's useful to compare them with more common investment vehicles. Mutual funds and Exchange-Traded Funds (ETFs) are effective tools, but they operate on a fundamentally different principle.

These are pooled investments. Buying into a mutual fund or ETF is like purchasing a ticket for a bus—you share the ride with everyone else and travel to a predetermined destination. A managed account, by contrast, is like hiring a private car. You set the destination, the route is customized for you, and you are the only passenger. This distinction creates significant differences in ownership, transparency, and control.

Ownership and Transparency: The Core Divide

The most significant difference comes down to the ownership of the underlying assets. When you buy shares in a mutual fund or an ETF, you own a piece of the fund itself, not the individual stocks or bonds it holds. The fund is the legal owner of those securities.

With a managed account, you directly own every single security in the portfolio. The stocks, the bonds, the crypto assets—they are all held in an account with your name on it. This provides a level of transparency that pooled funds cannot match. You see every holding, every trade, and every fee as it occurs.

This direct ownership unlocks several key advantages:

Granular Control: You can instruct your manager to avoid specific industries or companies that do not align with your values.

Clearer Reporting: Your statements show your actual holdings, not just a share price based on a fund's calculated Net Asset Value.

No Shared Risk: You are not affected by the actions of other investors. In a mutual fund, large-scale redemptions can force a manager to sell assets at an inopportune time, a problem that does not exist in a managed account.

Customization and Tax Efficiency

Because a managed account is built for a single investor, it can be fine-tuned with incredible precision. A manager can shape the portfolio not just around your risk tolerance but also your specific tax situation. This is where managed accounts are particularly advantageous, especially for high-net-worth individuals and family offices.

A key benefit of direct ownership is the ability to engage in tax-loss harvesting. Your manager can strategically sell individual securities at a loss to offset capital gains realized elsewhere in your portfolio, a technique that is impossible within the commingled structure of a mutual fund.

This type of tax-aware management can significantly improve after-tax returns over the long term. A mutual fund manager, by contrast, must manage for the entire pool of investors, which often means distributing capital gains to all shareholders, regardless of their individual tax situations.

To make this clear, here’s a straightforward comparison of these three structures across the features that matter most.

Managed Accounts vs Mutual Funds vs ETFs A Feature Comparison

This table breaks down the key differences between these popular investment structures to help you see which might be the right fit.

Attribute | Managed Account | Mutual Fund | ETF |

|---|---|---|---|

Asset Ownership | Direct (Investor owns individual securities) | Indirect (Investor owns shares of the fund) | Indirect (Investor owns shares of the fund) |

Customization | High (Tailored to individual goals and taxes) | Low (Standardized portfolio for all investors) | Low (Standardized portfolio for all investors) |

Transparency | High (Full visibility into all holdings) | Moderate (Holdings disclosed periodically) | High (Holdings disclosed daily) |

Tax Efficiency | High (Allows for tax-loss harvesting) | Low (Can distribute unwanted capital gains) | Moderate (Generally more tax-efficient than mutual funds) |

Minimum Investment | Typically Higher | Generally Low | Low (Price of one share) |

Ultimately, the right choice depends on your priorities as an investor. If you're looking for a low-cost, diversified, "set-it-and-forget-it" option, ETFs and mutual funds are powerful and effective tools. But for investors who require greater control, deep customization, and tax optimization, the managed account structure offers a compelling, personalized alternative.

From Separate Accounts to Integrated Platforms: An Evolution

The concept of a managed account is not new. It is the result of a long evolution, shaped over decades by investors seeking greater control, transparency, and strategies built for their specific needs.

This history begins with the classic Separately Managed Account (SMA). SMAs were the original bespoke solution in the investment world, a direct response to the standardized nature of mutual funds. For a detailed analysis, we have a complete guide on what Separately Managed Accounts are that explains the structure.

For a long time, SMAs were the primary choice for investors seeking a truly personalized portfolio. A manager would hand-pick stocks and bonds specifically for an individual. The challenge, however, was that this created isolated pools of capital. An investor might have one SMA for US equities, another for international bonds, and a third for an alternative strategy. Gaining a clear, holistic view of one's total wealth was a significant operational burden.

Bringing It All Together: The Rise of Unified Management

To solve this silo problem, the industry developed the Unified Managed Account (UMA). If an SMA is a single, tailored investment, a UMA is the master container designed to hold all of them. It allows an investor to house multiple strategies—different SMAs, mutual funds, ETFs, and other assets—all under one unified structure.

This represented a major leap forward for several key reasons:

A Holistic Portfolio View: For the first time, investors and advisors could see the entire financial picture and understand how all the different components were interacting.

Consolidated Reporting: The need to sift through paperwork from different managers was eliminated. All holdings and performance data were presented in a single, consolidated report.

Smarter Portfolio Adjustments: Rebalancing became a strategic exercise across the entire portfolio, not just a series of isolated adjustments within each silo.

This shift from SMAs to UMAs marked a pivotal moment, moving the industry toward a much more integrated and efficient method of managing wealth.

Technology was the real catalyst for this evolution. Sophisticated software made it possible to aggregate data, execute complex strategies, and deliver clear reports on a scale that was previously impossible. This is what truly democratized access to managed accounts.

The momentum has continued. The managed accounts industry has grown substantially, especially in markets like Australia where assets under management grew from $10 billion to $200 billion in just ten years. This growth was largely driven by financial advisors seeking better, more scalable ways to serve their clients within a strict compliance framework.

A major asset manager like BlackRock now offers model portfolios to over 1,400 advisors, covering everything from ESG-focused strategies to custom ETFs. This exemplifies the incredible variety and sophistication now available through modern managed account platforms. You can read more about the decade-long evolution of managed accounts and what's fueling their popularity.

The Good, The Bad, and The Essential

Is a managed account the right approach for you? To determine that, you need to look at the whole picture—the clear advantages and the real-world trade-offs. It is not a universally suitable solution, so weighing both sides is crucial.

The primary benefit, without a doubt, is customization. An ETF is analogous to buying a suit off the rack; it serves its purpose. A managed account is like commissioning a custom-tailored suit. The manager constructs a portfolio specifically for you, factoring in your risk tolerance, timeline, and even personal values or specific tax situations.

This direct ownership model also provides a crystal-clear view of your investments and powerful tax advantages. You see every single stock, bond, or asset you own and every transaction. Furthermore, a manager can sell individual losing positions to offset gains elsewhere, a strategy known as tax-loss harvesting. That is something you simply cannot do in a pooled fund, and it can make a significant difference to your after-tax returns.

Weighing the Trade-offs

Of course, that level of personalized service comes with a few considerations. The most common hurdle has historically been higher investment minimums. While technology is making managed accounts more accessible, they still typically require more capital to start than purchasing shares of a mutual fund.

Then there are the fees. Managed accounts typically charge a percentage of the assets they manage (AUM). This can seem high compared to the low expense ratios of a passive index fund. The value proposition is that the manager's expertise, custom strategy, and risk management will deliver enough value to more than offset the higher cost.

When you choose a managed account, you're not just buying a product; you are engaging a professional or a team. This requires due diligence. Analyzing a manager's track record, investment philosophy, and risk management processes is not just advisable—it's essential.

Gaining Ground in Mainstream Finance

Despite the trade-offs, managed accounts are no longer exclusively for the ultra-wealthy. They are quickly becoming a staple in mainstream investing, particularly for retirement planning.

In the U.S. alone, more than a third of all retirement plan sponsors now offer managed accounts to their employees. Even more telling, 16% of sponsors have made managed accounts the default investment option for new employees. That is a massive vote of confidence. You can examine the data yourself in the PLANSPONSOR Defined Contribution Benchmarking Report.

This shift demonstrates how far managed accounts have come—from a niche offering for the wealthy to a core component of modern financial planning.

Bringing Managed Accounts to the World of Digital Assets

The same principles that made managed accounts a staple in traditional finance—customization, transparency, and professional oversight—are now being applied to the digital asset space. For sophisticated allocators like high-net-worth individuals, family offices, and institutions, the managed account framework offers a robust, reliable structure to engage with advanced crypto strategies.

This goes beyond simple buy-and-hold investing. We are talking about accessing complex opportunities like DeFi yield farming or quantitative Bitcoin options trading, but without relinquishing custody of your assets. It's a structure that directly addresses the core issues that have kept institutional capital on the sidelines.

Tackling Crypto's Trust and Security Problem

Without question, the single greatest advantage of using a managed account for digital assets is how it mitigates counterparty risk. When you invest in a typical crypto fund, you send your Bitcoin and stablecoins to the fund manager’s wallet. With a crypto managed account, your assets remain in your own separate, professionally custodied account.

The manager is granted permission to trade on your behalf, but that is the extent of their access. They cannot withdraw your funds. This separation is a game-changer for security and offers crucial peace of mind in a volatile market.

This structure fundamentally changes the security dynamic. By retaining direct ownership and control over assets held with a qualified custodian, allocators can access alpha-generating strategies while minimizing the risk of asset commingling or fund mismanagement.

For any allocator serious about deploying capital into this new asset class, understanding asset protection is non-negotiable. We've compiled an in-depth guide on digital asset custody solutions that dives deep into how these frameworks deliver institutional-grade security.

A New Hub for Discovery and Due Diligence

Fortunately, you do not have to navigate this landscape alone. A new wave of specialized platforms is making it far easier for investors to find and connect with vetted crypto managers. Think of these platforms as a central hub where you can discover, research, and monitor different strategies, all in one place.

This brings a welcome dose of structure and professionalism to an often-chaotic space. These platforms provide tools for:

Strategy Discovery: You can filter managers based on your specific criteria, whether it’s Bitcoin-denominated credit, high-yield stablecoin strategies, or market-neutral derivatives.

Due Diligence: Obtaining reliable information can be challenging in crypto. These platforms provide verified performance data, risk metrics, and detailed strategy documents, making the manager vetting process much more rigorous.

Ongoing Monitoring: Once you've allocated capital, you receive consistent, transparent reporting. This lets you track performance in real-time and ensure the manager is adhering to the agreed-upon mandate.

Ultimately, this framework makes the managed account an essential tool for any allocator looking to put serious capital to work in the digital asset market with confidence and control.

Your Top Questions About Managed Accounts, Answered

Let's address a few of the most common questions investors have when they begin to research managed accounts.

Are Managed Accounts Only for the Super-Wealthy?

Not anymore. While they remain a natural fit for high-net-worth individuals and family offices requiring complex tax strategies or specific ethical investment mandates, the landscape has changed.

Modern platforms are making this structure accessible to a much broader group of investors. If you are an investor who values direct asset ownership and desires professional guidance that goes beyond a generic fund, a managed account could be a suitable option.

How Do the Fees Work?

Most managers utilize a straightforward fee model based on a percentage of the Assets Under Management (AUM). This typically ranges from 1% to 2% annually, though the exact figure can depend on the manager's reputation and the complexity of the strategy.

The benefit of this structure is that it aligns the manager's interests with yours—their compensation increases only when your account value grows. This is a very different dynamic from commission-based models where an advisor might be incentivized to trade more frequently.

Keep in mind, this fee covers more than just trading. It includes ongoing professional oversight, a customized strategy, and transparent reporting. The value proposition is that the benefits derived from this hands-on approach justify the cost.

Will I Lose Control Over My Investments?

Not at all. In fact, you retain a great deal of control. You are delegating the day-to-day buy-and-sell decisions, but you are the one who establishes the governing rules in the Investment Policy Statement (IPS).

You always own the underlying assets directly, and you can see every single position and trade in your account. The manager’s job is simply to execute the strategy within the strict boundaries you have approved.

Ready to explore the world of digital asset management? Fensory is an institutional-grade platform where you can discover, analyze, and connect with top-tier managers specializing in BTC and stablecoin strategies. Get the data-rich insights you need to allocate with confidence.